You sit at the kitchen island at eleven at night, the harsh blue glow of your laptop illuminating a mug of lukewarm chamomile tea. The house is completely quiet, save for the rhythmic hum of the refrigerator. You have finally decided to book that long-overdue flight to Honolulu. The dates are set, the hotel is picked, and you navigate to your credit card rewards portal, anticipating the deeply satisfying click of paying with the points you have meticulously hoarded for over two years. You remember every grocery run, every gas station fill-up, and every strategic dining purchase that contributed to this balance. But as the page loads, the balance suddenly reads zero. A cold knot forms in your stomach. The digital ghost town where seventy thousand miles once lived is a stark reminder of a harsh reality: you did not spend them, so the bank took them back.

The Illusion of the Permanent Piggy Bank

We treat our reward balances like family heirlooms. We stash them away with a sense of pride, assuming they are safely locked in a permanent digital vault, waiting patiently for the perfect anniversary trip or a sudden cross-country emergency. But holding points is more like renting a small apartment without a formal lease. You do not actually own the currency; you are merely occupying space on the bank’s massive corporate balance sheet. The landlord holds the right to change the locks at a moment’s notice, often burying this power deep within the legal jargon of an updated terms of service agreement.

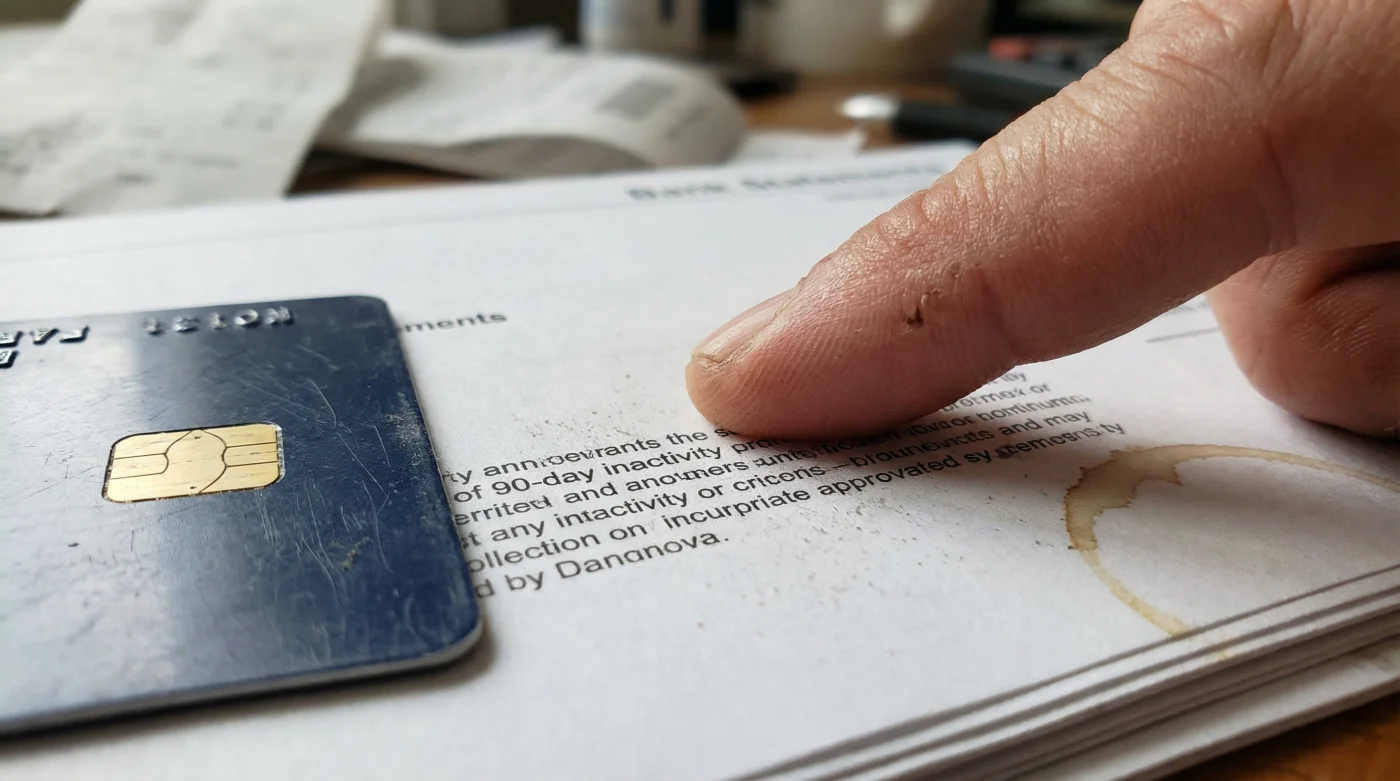

This is where the quiet, heavily automated machinery of the travel rewards industry operates. The widespread belief that earned reward points are permanently owned is the exact friction point banks rely on to balance their books. Instead of making loud, public announcements about stripping away your assets, they rely on a silent, relentless clock: the 90-day inactivity trigger. If your premium travel card sits dormant in a sock drawer for just three consecutive billing cycles, major financial institutions now quietly sweep your account clean. They bank on your forgetfulness.

I first learned about this ruthless efficiency from Marcus, a former rewards actuary based out of Chicago. We were sitting over black diner coffee on a freezing Tuesday morning when he took out a pen and sketched a card’s “burn rate” on a flimsy paper napkin. “People view points as a traditional savings account,” he said, tapping his pen against the paper for emphasis. “But banks view them as rapidly growing, unsecured financial liabilities. Every point you earn is a fraction of a cent they owe you. They are constantly searching the fine print for a legal, quiet way to erase that debt without losing you as a customer.” Marcus explained that as the economy fluctuates, issuers tighten their belts by accelerating these expiration triggers, counting on the fact that most consumers only check their balances when they are ready to travel.

| Traveler Profile | Rewards Strategy | Specific Benefit |

|---|---|---|

| The Occasional Flyer | Switch to flat cash-back cards. | Eliminates the anxiety of expiration entirely. |

| The Business Traveler | Use automated point-pooling with a primary card. | Consolidates balances to ensure constant account activity. |

| The Long-Term Hoarder | Attach the dormant card to a tiny, recurring subscription. | Creates an artificial heartbeat to keep the 90-day clock resetting. |

Keeping the Pulse Alive

Beating the 90-day trap does not require financial gymnastics, nor does it mean you have to use a premium card for your everyday expenses. It simply requires a mindful, deliberate adjustment to your monthly routine. The algorithm governing your points does not care if you spend five thousand dollars on a business class ticket or two dollars on a pack of peppermint gum at the corner store. It only searches for a pulse. A single, solitary transaction proves to the system that you are still actively engaged with the credit line.

To protect your hard-earned balance, physically take the forgotten travel card out of your drawer. Attach it to a low-cost, heavily automated charge. A monthly one-dollar pledge to a favorite creator on Patreon, a basic digital newspaper subscription, or even a fifty-cent iCloud storage fee is entirely enough to satisfy the ledger. Set the card to auto-pay directly from your primary checking account, and then you can safely put it back out of sight, knowing the system will do the heavy lifting for you.

- White vinegar permanently etches natural stone countertops during routine daily cleaning.

- USB-C cables destroy expensive laptop motherboards lacking this specific internal resistor.

- Hyaluronic acid dehydrates mature skin applied directly onto a dry face.

- Water heaters flood basement floors ignoring this crucial annual flushing requirement.

- Melatonin supplements disrupt morning alertness taken exactly at your standard bedtime.

| Card Activity | Algorithmic Logic | System Result |

|---|---|---|

| Zero transactions for 90 days. | Account flagged as abandoned liability. | Complete forfeiture of accumulated points. |

| Logging into the rewards portal. | Session recorded, but no financial movement detected. | Expiration clock continues ticking uninterrupted. |

| Purchasing a $2 coffee. | Financial ledger registers new active debt. | 90-day expiration timer resets entirely. |

Reclaiming Your Digital Wealth

This subtle shift in consumer habits is a massive wake-up call for anyone who casually collects miles. We spend years meticulously planning our spending, routing our groceries, gas, and holiday shopping through specific, high-fee cards just to earn a free vacation. Allowing a hidden technicality to wipe out years of that financial effort is a uniquely modern tragedy. You worked diligently for that monetary value, and protecting it is fundamentally an act of respecting your own time and money.

Do not let the system outsmart your routine. Review the terms of your current wallet immediately. Do not wait for a courtesy email warning you about an impending expiration date, because that email often never arrives, or it gets caught in an aggressive spam filter. Take a quiet Saturday morning to audit your accounts, set up your recurring micro-charges, and breathe easier knowing your next major vacation is actually secure and waiting for you.

| What To Look For | What To Avoid |

|---|---|

| Explicit “Points do not expire” clauses in the cardmember agreement. | Vague language like “Points may be forfeited upon account inactivity.” |

| Portals that allow free point transfers between family members. | Programs that charge a reactivation fee to restore expired points. |

| Generous grace periods of 18 to 24 months for legacy accounts. | Co-branded airline cards with strict, unchangeable 90-day triggers. |

“Your travel rewards are not a legacy; they are a highly perishable asset. Spend them, or manage them, before the bank decides they have spoiled.” – Marcus T., Former Rewards Actuary

Frequently Asked Questions

Can I call the bank to get my expired points back?

Sometimes, but it requires escalating the call to a retention specialist. If they do reinstate them, they often charge a steep penalty fee per point.Does paying an annual fee count as account activity?

Surprisingly, no. Most banking algorithms exclude annual fees from the transaction ledger that resets the inactivity clock.Do cash-back rewards expire the same way travel points do?

Generally, pure cash-back cards are far more lenient, and many do not expire at all as long as the account remains open and in good standing.How can I safely track expiration dates across multiple cards?

Third-party rewards management apps can sync your balances, but reading your specific cardmember agreement is the only completely foolproof method.Is it safer to transfer all my points directly to an airline?

Not always. Airlines have their own expiration policies, sometimes even stricter than the credit card issuers. Always verify the airline’s rules before moving your assets.